Introduction

The global healthcare landscape is rapidly evolving with the rise of precision medicine, where treatments are tailored to individual genetic profiles and disease characteristics. At the core of this transformation lies companion diagnostics (CDx)—a powerful class of diagnostic tools that help identify patients most likely to benefit from a particular therapeutic product. These diagnostics are playing a crucial role in optimizing drug efficacy, reducing adverse effects, and improving overall treatment outcomes.

Market Overview

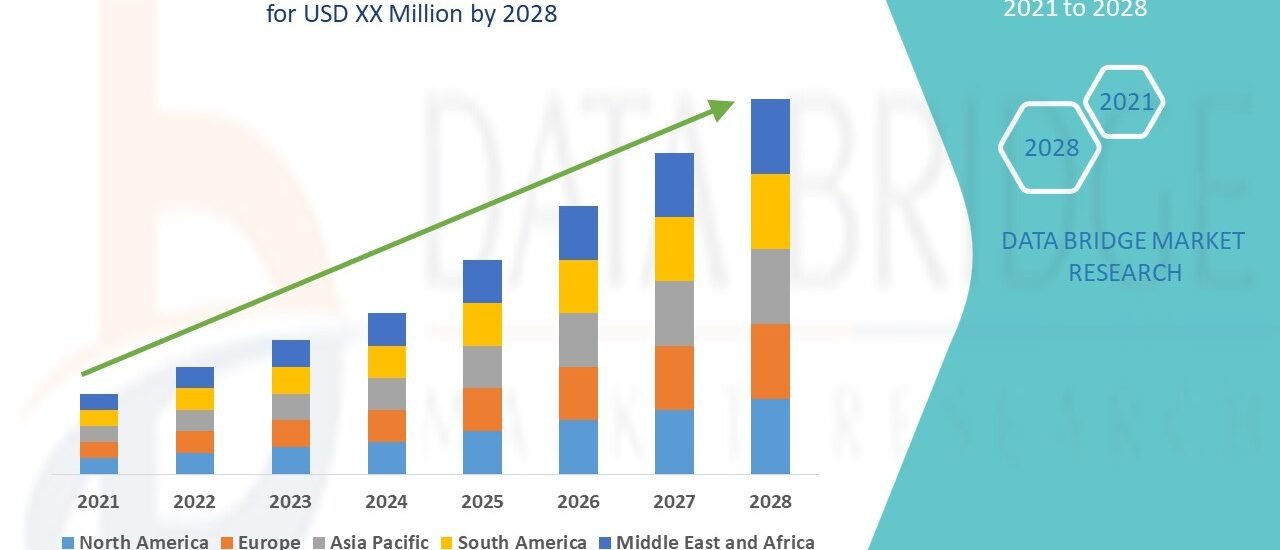

The global companion diagnostics market is witnessing robust growth and is expected to surpass USD 13 billion by 2030, growing at a CAGR of over 12% from 2024 to 2030. This growth is driven by the increasing demand for targeted therapies, the rising burden of cancer and chronic diseases, and the growing adoption of personalized medicine.

Pharmaceutical and biotechnology companies are increasingly partnering with diagnostic manufacturers to co-develop drugs and their corresponding tests, a trend that is accelerating innovation and regulatory approvals.

Key Market Drivers

-

Rise in Targeted Therapies: The proliferation of targeted therapeutics, especially in oncology, has necessitated the use of CDx tests to ensure patient suitability and treatment efficacy.

-

Technological Advancements: Innovations in genomics, next-generation sequencing (NGS), and digital pathology are expanding the capabilities and reach of companion diagnostics.

-

Regulatory Support: Regulatory bodies like the FDA and EMA are actively supporting CDx development through expedited approval pathways and updated guidelines.

-

Increasing Cancer Prevalence: With cancer becoming a leading cause of death globally, companion diagnostics are being used to identify specific biomarkers and guide treatment decisions.

Challenges and Restraints

Despite strong market potential, the CDx sector faces several challenges:

-

High Development Costs: Co-development of drugs and diagnostics requires significant investment in R&D and clinical trials.

-

Regulatory Complexity: Varying regulatory frameworks across regions can hinder global commercialization.

-

Limited Access in Emerging Markets: High costs and lack of infrastructure restrict adoption in low- and middle-income countries.

Segmentation Highlights

-

Indication: Oncology remains the dominant segment, particularly for breast cancer, lung cancer, and colorectal cancer.

-

Technology: Polymerase chain reaction (PCR) and NGS are the leading technologies, with NGS gaining ground for its high-throughput capabilities.

-

End-users: Hospitals and diagnostic laboratories are the primary users, although the role of academic and research institutions is growing.

Regional Insights

-

North America holds the largest market share due to a strong healthcare infrastructure, supportive regulatory policies, and a high adoption rate of precision medicine.

-

Europe follows, with Germany and the UK at the forefront of personalized healthcare initiatives.

-

Asia-Pacific is the fastest-growing region, fueled by increasing healthcare investments, government support, and rising awareness about genetic testing.

Competitive Landscape

Major players in the companion diagnostics market include:

-

Roche Diagnostics

-

Thermo Fisher Scientific

-

Qiagen N.V.

-

Agilent Technologies

-

Illumina, Inc.

-

Abbott Laboratories

These companies are investing heavily in partnerships, acquisitions, and R&D to strengthen their portfolios and expand global presence.

Future Outlook

The companion diagnostics market is poised for sustained growth as the global shift toward personalized medicine continues. With emerging technologies, improved regulatory clarity, and expanding clinical applications beyond oncology (such as autoimmune diseases and CNS disorders), the next decade is set to witness a revolution in how diagnostics and therapeutics are integrated.

Get More Details:

https://www.databridgemarketresearch.com/reports/global-companion-diagnostics-market

Conclusion

Companion diagnostics are not just tools—they are enablers of a future where medicine is more precise, efficient, and patient-centric. Stakeholders across the healthcare ecosystem must collaborate to overcome existing barriers and fully harness the potential of this transformative field.